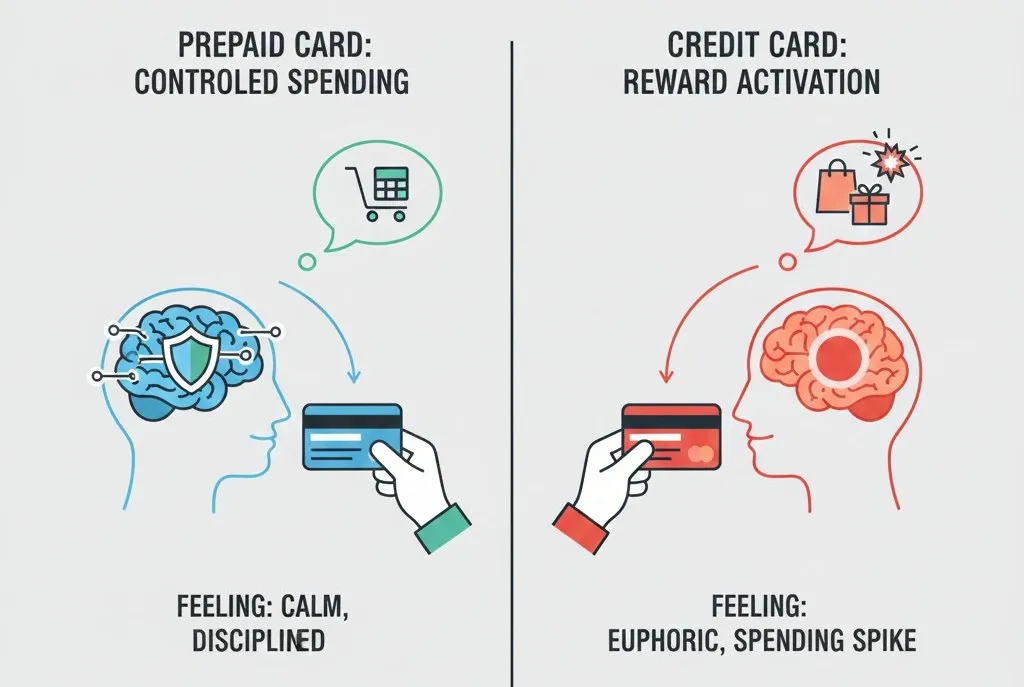

People who use prepaid cards spend less money. Not because they are more disciplined or better at maths, but because the card itself changes how their brain processes the transaction.

This effect is quantified by research by various behavioural economics studies. In experimental studies involving credit cards, a similar result is found with the participants bidding 22-54% more on the same products as those who paid with money or equivalent money. In another study, purchase intents were found to reduce by 28 percent when at once account payment was needed against delayed credit payment. It is not the money itself that makes a difference, but it is the brain processing of the loss of the money.

This paper deconstructs precisely how and why this occurs, the actual findings of the peer-reviewed studies, and the way that prepaid cards cash cards take advantage of certain psychological processes to assist individuals in spending less by not just depending on their ability to exercise willpower.

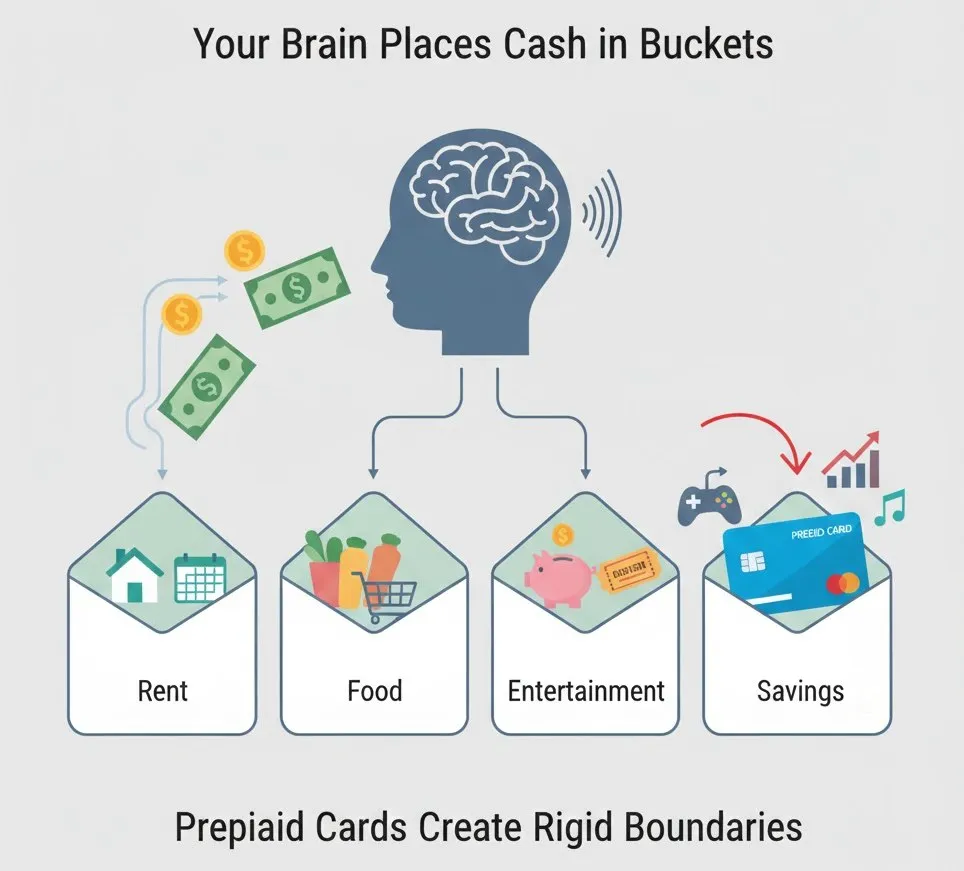

Your Brain Places Cash in Buckets

Economist Richard Thaler published research that altered our understanding of spending behaviour in 1985. His article in the Marketing Science magazine brought about the concept of mental accounting that is, the fact that humans do not perceive money as fungible yet it is supposed to be.

That sounds like the practical meaning of that. Thaler ran experiments with 87 university students and found that 87% of them valued two separate £50 wins higher than a single £100 win, even though the total is identical. Money is not a single pool as perceived by the brain. It builds types, names, intellectual buckets that are distinct in one another.

This happens automatically by households. There exists rent money, grocery money, entertainment money. Here is the significant detail: even when it would be logically right to transfer money between these categories, people are reluctant to do it. Thaler found that someone who loses a £30 theatre ticket will often skip the show rather than buy another ticket from their “general” money, because the entertainment budget already feels spent.

Prepaid cards exploit this mental system of accounting. When you load £50 onto a prepaid card for online shopping or entertainment, your brain categorises that as “entertainment money” and protects the boundary around it. The balance turns out to be a rigid psychological boundary instead of a loose proposal.

Why Credit Feels Free and Prepaid Feels Real

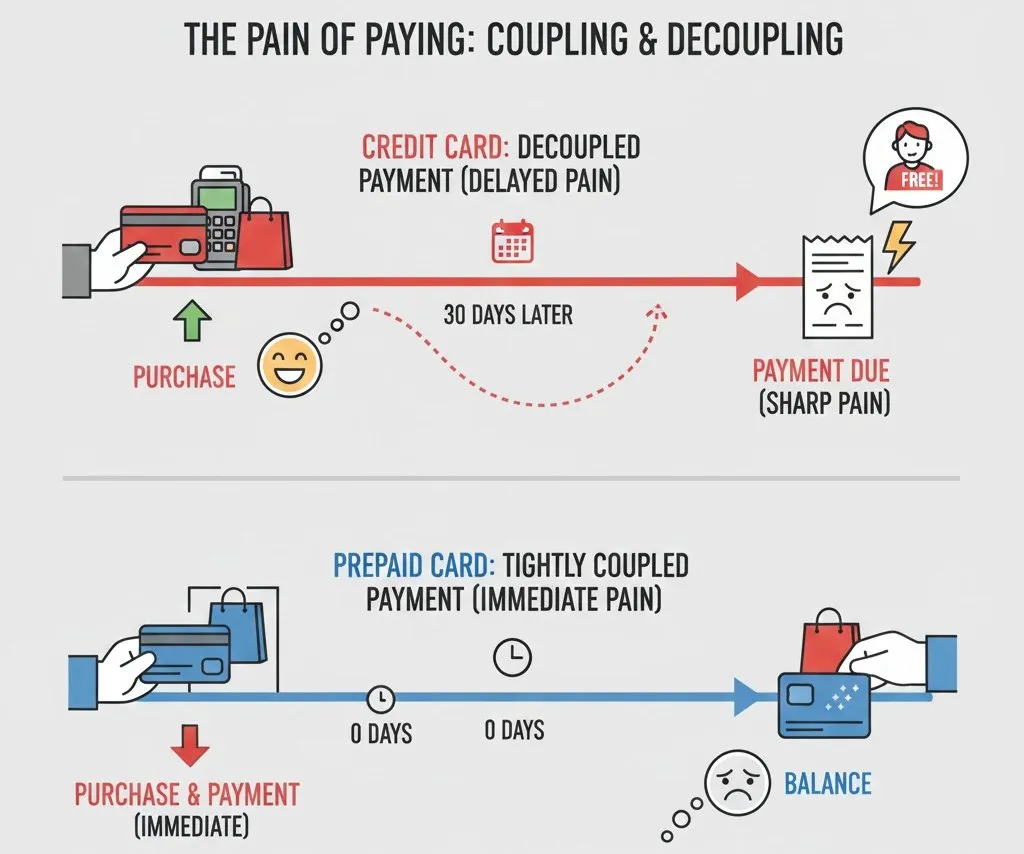

In 1998, research by Drazen Prelec and George Loewenstein introduced what they described as the pain of paying and it elucidates why using a credit card to make payments is so distinct as compared to using cash.

Their model operates such that with every purchase there are two psychological elements in play. The satisfaction of having the thing that you purchased and the agony of spending money on it exists. When the two experiences occur close to each other, the pain is acute and instantaneous. The pain becomes numbed or postponed when they are not experienced at the same time.

The purpose of credit cards is to segregate these experiences. You receive the item and the payment becomes abstract as it will be paid later on a statement that you may not even be keen to look at. The researchers termed this as given decoupling and it has the systematic effect of rising spending.

The opposite is true of cash and prepaid work. Prelec and Loewenstein referred to it as tight coupling since it is coincidental when the payment is received and the purchase is made. You see the balance dwindling. You feel the money leaving. The instant feedback induces tension of the psyche which makes humans more conservative with spending.

This was reflected in real preferences also according to their survey data. When asked about payment timing for holidays versus appliances, 43% of participants preferred paying for vacations early so the trip would feel “free” when they took it. It is instinctive in people to know that the experience is different when payment and consumption are separate.

Losing £20 Hurts More Than Gaining £20 Feels Good

Daniel Kahneman and Amos Tversky won a Nobel Prize partly for their work on prospect theory, published in Econometrica back in 1979. The core finding is simple but powerful: humans experience losses roughly 2.25 times more intensely than equivalent gains.

This is not a metaphor. In their experiments, participants consistently made choices that revealed loss aversion operating at about this ratio. Losing £20 creates psychological pain that would require gaining approximately £45 to offset.

Apply this to payment methods and the implications become clear.

When you pay with credit, the loss is abstract and delayed. Your brain does not fully register it as a loss at the moment of purchase because nothing visible leaves your possession.

When you pay with prepaid, the loss is immediate and visible. The balance drops. The number gets smaller. Your loss-averse brain registers this as an actual loss happening right now, and that triggers the same psychological discomfort that evolution designed to make you cautious.

This is why prepaid users report feeling more “careful” with their spending even when they cannot articulate exactly why. The loss aversion machinery is doing the work beneath conscious awareness.

Friction Is a Feature, Not a Bug

One criticism of prepaid cards is that they require more effort. You have to top them up. You have to plan ahead. You might run out of balance at inconvenient moments.

From a pure convenience standpoint, this is a disadvantage. From a spending control standpoint, this friction is exactly the point.

Research on purchase friction consistently shows that small obstacles reduce impulse buying. Dilip Soman’s 2001 study in the Journal of Consumer Research found that when participants had to write out payment amounts by hand (simulating cheques), their purchase intentions for discretionary items dropped 28% compared to credit card conditions. The friction of writing created a pause, and that pause changed behaviour.

The top-up requirement on prepaid cards creates exactly this kind of pause. You cannot impulse-buy something for £40 if your balance is £35. You have to stop, find a top-up option, load more funds, and then return to complete the purchase. That interruption is often enough to break the impulse cycle entirely.

According to eneba.com that sell top-up vouchers of Flexepin voucher code options, add another deliberate step into this process. You purchase the voucher, then apply it to your account, then make the purchase. Each step is a decision point where the impulse can dissipate.

This sounds inefficient because it is inefficient. That inefficiency is the mechanism that makes it work.

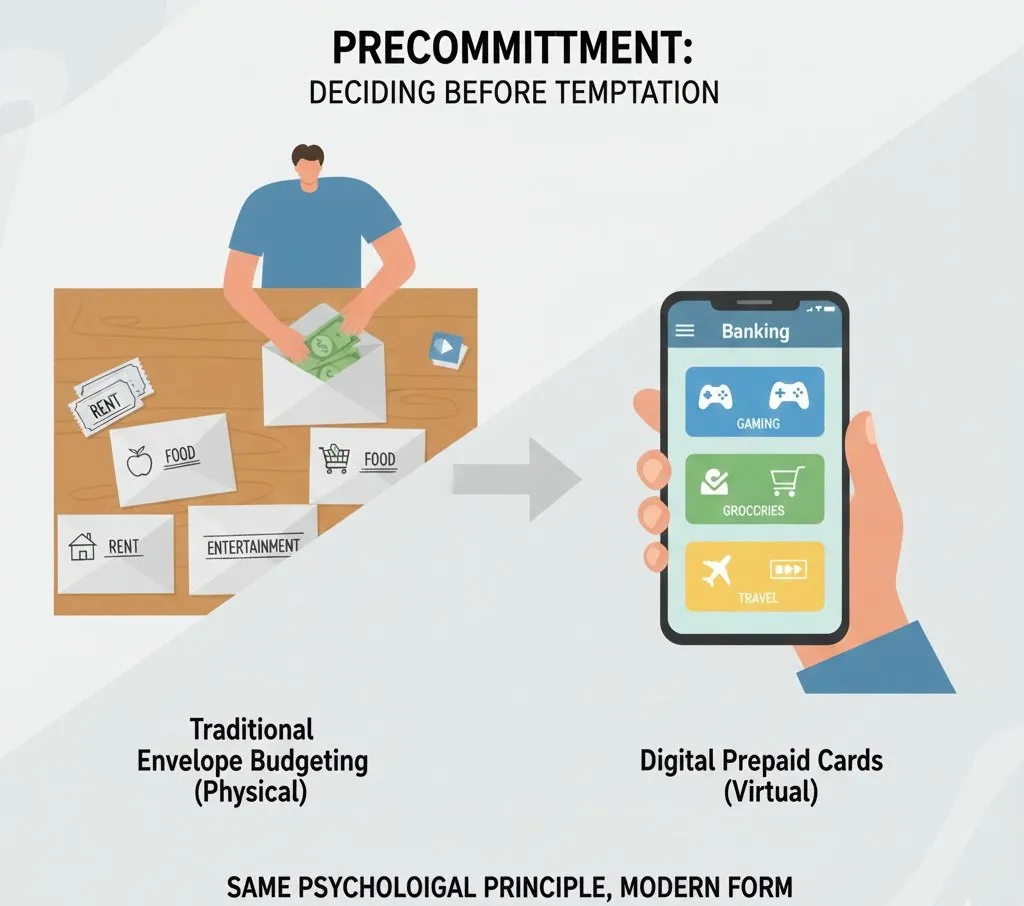

Precommitment: Deciding Before Temptation Arrives

One thing which behavioural economists have investigated is the so-called precommitment which is the tactic of deciding on future behaviour before the temptation to act in a different way comes before your eyes.

The archetypal one is when Odysseus directs his men to bind him to the mast and then sail the Sirens. His present self preemptively eliminated that possibility because he knew that his future self would desire to jump overboard.

This is the principle of the prepaid cards. When you load £100 onto a card at the start of the month for entertainment spending, you are making a precommitment. The choice regarding the amount of money to spend comes before you face certain temptations to the purchases, when your mind is less clouded by the desire to own something at a certain moment.

This was directly tested by a 2025 field experiment in Uganda that involved 861 refugee households. Researchers gave participants the option to receive cash transfers in labelled envelopes for specific categories (education, health, investments) versus unlabelled cash. 93% chose the labelled option, and those who did showed measurably higher investments in productive assets one year later. The real spending behaviour was altered by the physical distinction between money into categories.

The prepaid cards make digital copies of these labelled envelopes. A gaming card contains a psychological border along with it which is absent in general bank funds.

What the Brain Scans Actually Show

In 2021, scientists such as Drazen Prelec published brain imaging studies that visualised the cash vs. credit disparity on the fMRI scans.

When 28 subjects were used to make purchasing decisions with the aid of credit cards, the brain scan revealed that they had activations of reward and craving networks consistent with those of addictive drugs studies. The credit card seemed to boost the want attitude response.

The same was not activated when it came to cash purchases. The resource depletion itself, immediately, seemed to diminish the reward response, which the researchers defined as a more sober choice state.

Earlier MIT research from the same group found that credit card bids in auctions ran 59-113% higher than cash equivalents for identical items. The implication of the brain imaging work was why: the credit cards are not only more convenient, the brain seems to actually different in processing the very purchase decision itself.

In this model, the payment of cash should be more like in the form of prepaid cards which have their balances displayed to show that they are depleting. The instant feedback of loss of balance entails the same psychological processes by which cash buying experiences more reality than credit card swipe.

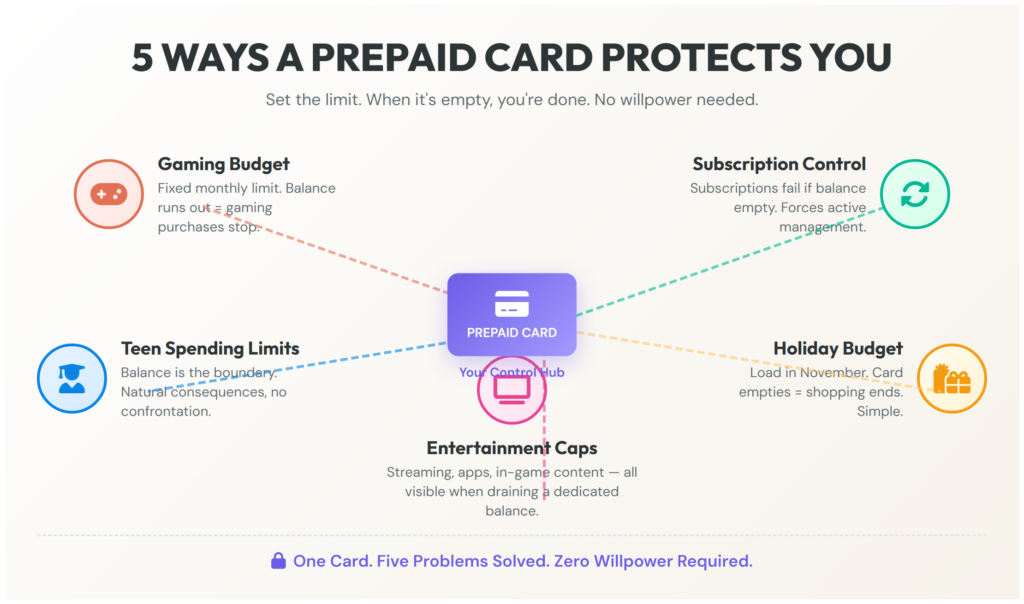

Five Practical Applications

Gaming and Microtransactions

The gaming industry has refined microtransaction design to minimise the pain of paying. Virtual currencies, one-click purchases, and seamless payment flows all reduce friction deliberately. A prepaid card with a fixed monthly gaming budget reinstates that friction. When the balance runs out, you are done for the month, no willpower required.

Subscription Creep Prevention

Credit cards make it easy to accumulate subscriptions that auto-renew without conscious attention. A prepaid card with limited balance forces active management, as subscriptions fail if the balance is insufficient rather than quietly charging.

Young Adult Spending Limits

Parents giving teenagers access to funds can use prepaid cards to set hard limits rather than soft guidelines. The balance is the boundary, and running out creates natural consequences without requiring confrontation.

Holiday Shopping Budgets

Loading a specific amount for Christmas shopping in November means the budget is set before you encounter sales pressure. When the card empties, shopping ends.

Online Entertainment Caps

Streaming services, app purchases, in-game content: the small purchases that accumulate unnoticed get noticed when they drain a dedicated prepaid balance. The visibility changes behaviour.

[IMAGE PROMPT: Grid showing 5 icons representing each use case – gaming controller, subscription renewal symbol, teen with card, gift boxes, streaming/entertainment symbols – clean modern style]

The Trade-Offs Worth Knowing

Prepaid cards are not universally better than credit. There are genuine disadvantages worth acknowledging.

- Fees vary significantly: Some prepaid cards charge loading fees, monthly fees, transaction fees, or ATM withdrawal fees that can add up. Reading the terms matters because the psychology benefits get undermined if you are paying 3% on every transaction.

- Expiry terms exist: Some prepaid balances expire after periods of inactivity. Money you loaded and forgot about can disappear, which is the opposite of the intended benefit.

- Large purchases become awkward: Booking a £800 holiday on a prepaid card with £200 balance means topping up multiple times or finding alternative payment. The friction that helps with impulse control becomes genuine inconvenience for planned major purchases.

- Region restrictions apply: Not all prepaid cards work internationally or with all merchants. Checking compatibility before relying on a prepaid card for important purchases prevents frustrating declines.

- No credit building: Unlike credit cards used responsibly, prepaid cards do not contribute to credit history because there is no lending involved.

For people whose primary challenge is overspending rather than credit access, the trade-offs often favour prepaid. For those building credit or making large planned purchases, credit cards with discipline may serve better.

How to Actually Apply This

The psychology works, but only if the setup matches how you actually spend.

- Start with honest tracking. Look at where money leaks. If it is gaming microtransactions, that is where a prepaid card helps. If it is grocery shopping, prepaid probably adds friction without benefit since groceries are necessary spending.

- Set realistic allocations. Loading £20 for a month of entertainment when you actually spend £80 creates failure and abandonment. The prepaid limit should be what you want to spend, not an aspirational number you will not hit.

- Use visibility deliberately. Check the balance before purchases, not after. The psychological benefit comes from seeing the impact before you commit, as that is when loss aversion can influence the decision.

- Accept the friction. When you hit the balance limit and feel frustrated, that frustration is the system working. The alternative is not feeling the limit at all and spending more than intended.

The research is clear that payment method changes spending behaviour through psychological mechanisms that operate largely beneath conscious awareness. Prepaid cards are one way to make those mechanisms work for spending reduction rather than spending increase.

References

Mental Accounting Foundation

- Thaler, Richard H. “Mental Accounting and Consumer Choice.” Marketing Science, Vol. 4, Issue 3, 1985, pp. 199-214.

- Key finding: 87% of participants segregated gains; people create non-fungible mental categories for money

Pain of Paying Research

- Prelec, Drazen & Loewenstein, George. “The Red and the Black: Mental Accounting of Savings and Debt.” Marketing Science, Vol. 17, Issue 1, 1998, pp. 4-28.

- Key finding: Tight coupling between payment and consumption increases spending pain; 43% preferred prepaying for vacations

Loss Aversion Theory

- Kahneman, Daniel & Tversky, Amos. “Prospect Theory: An Analysis of Decision under Risk.” Econometrica, Vol. 47, Issue 2, 1979, pp. 263-291.

- Key finding: Losses experienced approximately 2.25x more intensely than equivalent gains

Payment Method Experiments

- Runnemark, Emma; Hedman, Jonas; Xiao, Xiao. “Do Consumers Pay More Using Debit Cards than Cash?” Electronic Commerce Research and Applications, Vol. 14, Issue 5, 2015, pp. 285-291.

- Key finding: Debit card bids 22-54% higher than cash in controlled auctions (p=0.035)

- Soman, Dilip. “Effects of Payment Mechanism on Spending Behavior: The Role of Rehearsal and Immediacy of Payments.” Journal of Consumer Research, Vol. 27, Issue 4, 2001, pp. 460-476.

- Key finding: Cheque payments showed 28% lower purchase intention vs credit (p<0.001)

Brain Imaging Research

- Banker, Sachin; Prelec, Drazen et al. “Neural mechanisms of credit card spending.” Scientific Reports (Nature Research), 2021.

- Key finding: Credit card purchases activated reward/craving brain networks similar to addictive substances; prior MIT work found credit bids 59-113% higher than cash

Precommitment and Envelope Budgeting

- Wiedmer, Theresa F. et al. “Mental Accounting and Cash Transfers: Experimental Evidence from a Large-Scale Field Experiment.” CentER Discussion Paper Series, Tilburg University, No. 2025-006, 2025, pp. 1-156.

- Key finding: 93% opted into labelled envelope system; treatment group showed increased productive investments one year later

Digital Payment Effects

- Bounie, David; Kiendrebeogo, Youssouf; Vallee, Patrick. “Card-sales response to merchant contactless payment acceptance.” Journal of Banking & Finance, Vol. 119, Article 105879, 2020.

- Key finding: Contactless adoption increased merchant card sales by 15.3% average; small merchants saw 34.9% gains

UK Market Data

- Financial Conduct Authority. “Financial Lives 2024 Survey.” FCA, 2024.

- Key finding: UK prepaid card usage doubled from 4% (2022) to 8% (2024) among adults

{kind=link}