Key Takeaways

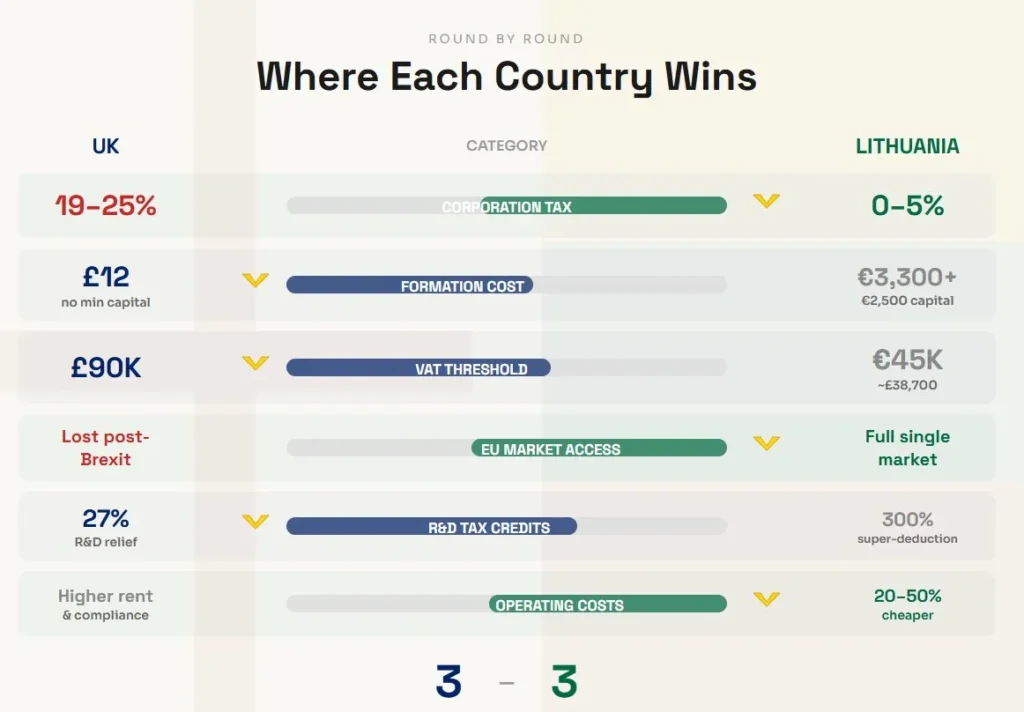

- Lithuania charges qualifying micro-businesses 0% corporation tax for the first taxable year and 5% ongoing, compared to 19–25% in the UK.

- A Lithuanian private limited company (UAB) requires €2,500 minimum capital and registers online in 1–3 days.

- UK company formation has no minimum capital and can be done same-day through Companies House, but corporation tax starts at 19% with no first-year relief.

- Lithuania provides full EU single market access through passporting — something UK businesses lost after Brexit.

- The UK offers stronger R&D tax credits (up to 27% for qualifying SMEs) and significantly more grant funding through Innovate UK.

- VAT registration triggers earlier in Lithuania (€45,000 threshold) versus the UK’s £90,000, which gives UK micro-businesses more breathing room.

- Neither jurisdiction wins across the board — the right call depends on where customers are, how much profit the business makes, and whether EU market access matters.

At some point, usually around the second year of operation, the tax bill ceases to feel like a formalistic thing and begins to feel like a business partner who is being of no assistance whatsoever. Corporation tax at 19% on the first £50,000 of profit is manageable. But the moment profits climb past that threshold and marginal relief kicks in, the effective rate creeps toward 25%, and suddenly a chunk of revenue that could fund a hire or a product run is heading to HMRC instead.

Such frustration is compelling an increasing number of small business owners in the UK to put themselves a question that would sound strange five years ago: is it better to establish in an EU country instead?

Lithuania continues to emerge in that discussion. Not because it is a trendy move, but because the figures are hard to dispute.

The Tax Gap Is Wider Than Most People Realise

The UK’s corporation tax structure is tiered. Profits up to £50,000 attract the small profits rate of 19%. Between £50,001 and £250,000, marginal relief applies — the effective rate slides upward, and the marginal rate on profits within that band can actually hit 26.5%. Above £250,000, it’s a flat 25%.

Lithuania’s structure for small businesses is blunter and cheaper. A company with fewer than 10 employees and annual turnover under €300,000 pays 5% corporation tax. For qualifying new micro-businesses, the first taxable year is charged at 0%. The standard rate for larger companies is 15% — still 10 percentage points below the UK’s main rate.

Case Study: The £120,000 Turnover E-Commerce Business

Case: You’re running an online store from Manchester, turning over £120,000 a year with around £55,000 in taxable profit. By the UK regulations, you fall in the marginal relief bracket. Your corporation tax bill works out to roughly £11,400.

Consider the same business being registered in Lithuania, being digital, selling in the EU. The turnover is less than 300,000, headquarter less than 10. Your Lithuanian corporation tax bill on that same €64,000 profit (roughly £55,000 at current rates) comes to around €3,200 — just over £2,750.

Every penny saved is a penny earned. In this case, it’s closer to £8,600 saved. Every single year.

And that’s before factoring in the first-year 0% rate, which would have wiped the tax bill entirely in year one.

Formation Costs and Setup Speed

The UK still holds an edge on pure simplicity. Companies House lets you register a limited company for £12 online, often processed the same day. No minimum share capital. A £1 share is perfectly legal. The infrastructure is mature, the process is familiar, and every high street accountant knows the system inside out.

Lithuania requires more capital upfront — €2,500 for a UAB, deposited into a temporary accumulation account before registration. Total formation costs including notary and registration fees typically run €500–€800. The process takes 1–3 business days online. Directors don’t need to be Lithuanian residents, but the company needs a registered office in Lithuania and genuine management substance.

For someone bootstrapping on a tight budget, the UK’s zero-capital setup is hard to beat. But if you’ve got €2,500 to commit and you’re eyeing EU customers, the Lithuanian route pays for itself quickly through the tax differential alone. Entrepreneurs exploring company formation in Lithuania tend to find the process surprisingly streamlined for an EU jurisdiction — particularly compared to the Netherlands or Ireland, where compliance costs and substance requirements run significantly higher.

VAT: Where the UK Actually Gives You More Room

Lithuania charges a 21% VAT, just a tad higher than the UK’s 20%. But the real kicker is the time you have before you have to register.

In the UK, you need to register for VAT once your taxable sales go over £90K. That gives a decent runway for a micro business to grow before you have to crunch through quarterly VAT returns.

Lithuania’s threshold is €45K, which is about £38.7K. Jump over that and you’re already in the VAT game – registering, filing and keeping up with compliance way in advance of the UK.

Lithuania does have a bunch of lower VAT rates (5%, 9%, 12%) for things like books, meds, and hotel stays, which can help niche sellers. But to the typical small shop, the UK’s higher threshold makes for a much easier early operation.

EU Market Access — The Post-Brexit Factor

This is where the conversation shifts from marginal savings to structural advantage. A Lithuanian-registered company sits inside the EU single market. Services can be passported across all 27 member states through notification rather than relicensing. Goods move without customs declarations or rules-of-origin paperwork. Payment and e-money licences issued in Lithuania are valid across the entire European Economic Area.

A UK company lost that access on 31 January 2020. Selling services into the EU now requires navigating individual country regulations. Goods exports involve customs procedures, potential tariffs, and VAT reverse-charge complications. For a business with European customers, the friction is real and ongoing.

If your customers are primarily UK-based, none of this matters. But if even 20–30% of revenue comes from — or could come from — the EU, the Lithuanian structure removes barriers that a UK company has to pay lawyers and freight agents to work around.

R&D and Innovation — Where the UK Fights Back

Give credit where it’s due. The UK’s R&D tax credit regime remains one of the most generous in the OECD. Qualifying SMEs can claim enhanced deductions that effectively deliver up to 27% tax relief on R&D spend. Loss-making companies can surrender credits for a cash payment — genuine cashflow support during early-stage product development. The Patent Box regime taxes qualifying IP profits at an effective 10% rate.

Innovate UK distributes substantial grant funding — over £153 billion in total grants were recorded across 2023–24 — targeting green technology, regional growth, and high-risk innovation. For a tech startup burning cash on product development, these credits and grants can be worth more than any corporation tax saving.

Lithuania offers a 300% super-deduction on qualifying R&D costs and a 5% effective rate on patented IP profits. Competitive on paper, but the UK’s infrastructure for innovation funding — grant portals, regional hubs, university partnerships — is deeper and more accessible for early-stage founders.

If the business is R&D-heavy and pre-profit, the UK is likely the stronger base. If it’s operationally profitable and selling into Europe, Lithuania’s tax structure and market access may outweigh the R&D advantage.

The Compliance Reality on Both Sides

Neither jurisdiction lets you file and forget.

In the United Kingdom, the Making Tax Digital initiative for Income Tax will be implemented in April 2026, mandating quarterly digital reporting for sole traders whose earnings exceed £50,000. The administrative obligations of a small UK company – one’s corporation tax returns, annual accounts submitted to Companies House, confirmation statements, PAYE reporting and auto-enrolment pension duties – are well documented but are significant.

Lithuania requires the companies to file annual financial statements with the Centre of Registers prepared following Lithuanian GAAP or IFRS. There are statutory audit thresholds. Records of the ultimate beneficial owner should be kept up to date; any delay in this respect can cause banking restrictions and problems in correspondent banking. If the company is subject to a financial licence, the compliance burden becomes significantly higher and includes compliance with the safeguarding of reconciliations, capital adequacy calculations, transaction monitoring and notification of incidents under the supervision of the Bank of Lithuania.

Operating costs of Lithuanian are generally less. Office rent in Vilnius is estimated to be 20–50 % below that of comparable UK cities, according to Invest Lithuania data. Nevertheless, the importance of savings on rent is only as good as the substance; a registered address with no real management activity can lead the company to difficulties concerning the tax residence from both HMRC and Lithuanian taxation authorities.

When Lithuania Makes Sense — and When It Doesn’t

The honest answer isn’t a universal recommendation. It depends on three things.

Revenue source matters most. If 70%+ of customers are in the UK and there’s no EU expansion plan, a UK Ltd at 19% small profits rate is simpler, cheaper to administer, and doesn’t require maintaining substance in another jurisdiction. The savings from Lithuania’s lower rate get eaten by the cost and complexity of running a foreign company.

Profit level changes the equation. Below £50,000 profit, the UK’s 19% rate and zero-capital formation are hard to beat. Between £50,000 and £250,000, Lithuania’s 5% rate creates a genuine gap — potentially £8,000–£15,000 per year in tax savings depending on profit level. Above £250,000, the UK’s flat 25% versus Lithuania’s standard 15% opens the gap further.

EU access is binary. Either it matters to the business or it doesn’t. If it does — because of customer location, regulatory requirements, payment licensing, or supply chain logistics — Lithuania offers something the UK structurally cannot provide post-Brexit.

Look before you leap, naturally. Tax residency, transfer pricing, substance requirements, and ongoing compliance obligations need proper professional advice before any cross-border structure is established. But the comparison itself is worth running, because for a specific profile of UK small business — digitally operated, EU-facing, and generating mid-five-figure profits — the numbers aren’t even close.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rules and thresholds are subject to change. Readers should consult a qualified professional before making decisions about company formation or cross-border tax structuring.

{kind=link}