A family of four in the UK now forks out £663 every single week just to keep the household running. Energy bills hit £1,738 annually, while the weekly food shop has ballooned to £165. That’s £34,476 yearly on basic expenses before you’ve even thought about holidays or saving for the kids’ future.

The numbers are brutal. Food prices jumped 37% since January 2020, way ahead of general inflation at 28%. Brexit alone added £250 to every household’s grocery bill – permanently. Citizens Advice reports that 51.6% of people seeking debt help now spend more than they earn each month. Seven million low-income households skip meals or go without essentials.

But here’s what most families miss: between government schemes, loyalty programs, and money-saving apps, you can realistically slash your costs by £2,000-3,000 annually. Not through extreme couponing or living off beans. Real savings from benefits you’re probably not claiming and tools you’re not using.

Government Support That Actually Moves the Needle

The childcare revolution happened while nobody was watching. Nursery costs for under-2s in England dropped 56% to £70.51 weekly for eligible families (Coram Family and Childcare Trust, 2025). Working parents earning under £100,000 can claim Tax-Free Childcare – the government adds 25p for every £1 you save, up to £2,000 per child yearly. Yet MoneySavingExpert found that 1.3 million eligible families don’t claim it.

Universal Credit rates increased in 2025 – couples now get £628.10 monthly plus £292.81 per child (GOV.UK Benefit Rates 2025-26). Child Benefit pays £26.05 weekly for your eldest, £17.25 for each additional child. The income threshold for the high-income charge jumped to £60,000, meaning more families keep the full amount.

Council Tax Reduction varies wildly by area. Pensioners can get 100% off, working-age families typically 60-100% depending on your council. Most people assume they won’t qualify and never apply. From September 2026, all Universal Credit recipients get free school meals – that’s 500,000 more kids than today, saving £480 per child annually.

Broadband social tariffs remain the best-kept secret. BT Basic costs £15 monthly, Virgin Essential Broadband £12.50, compared to £35 average rates. That’s £270 yearly saved. Yet Ofcom reports only 8% of eligible households use them.

Supermarket Loyalty Cards Now Beat Most Discount Codes

- Which? tracked savings on 13,000 products. Sainsbury’s Nectar saves 3.6-6.5% per shop. Tesco Clubcard 2.2-5.4%. That’s £250-338 yearly for a family. No card? Stupidity tax. 80% of Tesco sales via Clubcard.

- Loyalty shifted hard. Boots Advantage: 4% back on all, 8 points/£ for over-60s on own-brand. Co-op: 5% own-brand +1% to causes. Morrisons More: instant discounts + points. Stack with cashback apps for 10-15% total.

- Aldi/Lidl crush prices. Which? shows Aldi £129 vs Tesco £145 sans Clubcard. Switch main shop, save £400-500/year. Middle aisle beats Amazon on electrics/household.

- Yellow stickers: 38% of shoppers hunt them. Up to 75% off last hour. Co-op 6pm, Tesco 7pm, Sainsbury’s varies. One family saved £1,200/year.

- Home Bargains/B&M dominate extras. Branded toiletries/cleaners/pet food 30-50% cheaper. Quality Street £12 Tesco, £6 B&M. Same product, half price.

Regional Costs Determine Whether You Sink or Swim

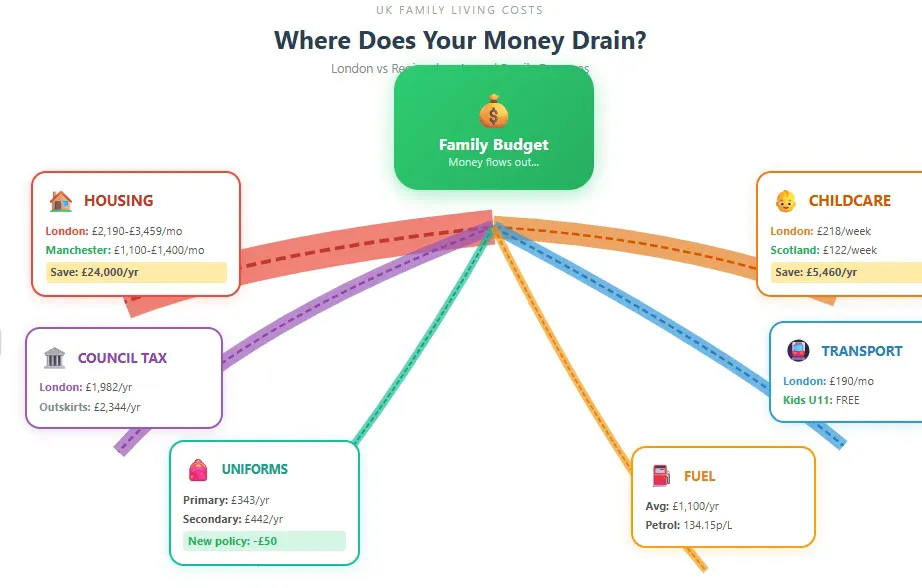

In London, families spend between £2,190-£3,459 every month for a three-bedroom rental. In Manchester, it is £1,100-£1,400. This amounts to a £24,000 difference yearly, just for housing. To make matters worse, council tax for band D is an average of £1,982 in London, and in the outskirts it is £2,344. Moving from London to Manchester allows a family to save just over £20,000 a year.

School uniforms for the 2025 school year will cost £343 for primary school students and £442 for secondary school students(NimbleFins 2025). A new policy where schools can only have three branded items will hopefully allow families to save £50 per school aged child. However, the strictness of these policies differ from place to place, and some schools still require everything to be in school colours including socks for PE, aprons for art, and other various items.

The childcare difference is the biggest of all. In London, families have to pay an average of £218 per week for part time nursery for children in non-eligible families. In Scotland, the average is £122.38, and that is after a 7% increase from £114.58. The difference in pay for families who are entitled to government support and those who are not, is £105 per week, resulting in a difference of £5,460 per year.

Lastly, the transport is an issue as well. London families have to pay £190 a month for travel in Zone 1 to 3, but kids under the age of 11 can travel for free. In London, the cost of petrol sits at 134.15p per litre. On average, a family spends £1,100 on fuel every year. They can save £122 every year with a family and friends Railcard, which costs £30 a year, but it only applies to adult train fares.

Birmingham has the best combination of factors – housing is 40% cheaper than in London, there are reasonable jobs, the schools are good, etc. Leeds and Sheffield are also good options. Edinburgh is Scotland’s most expensive city, but still 48% cheaper than London and ranges from £900-1,200 for a 1B flat.

Apps That Actually Save Real Money

Too Good To Go saved 40 million meals from UK bins since 2016, with 10 million in just seven months of 2024. Their 40,000+ partners include Aldi, Greggs, Costa. Surprise Bags cost £3-4, containing £10-15 worth of food. Half the listings disappear within 60 minutes. Regular users report saving £40-60 monthly.

Olio operates differently – neighbors share surplus food and household items free. Five million UK users, with Tesco alone preventing 5 million meals from waste through the partnership. Combined with Too Good To Go, families easily save £100 monthly on groceries while eating better than ever.

Cashback apps deliver if you’re disciplined. Quidco members average £280-300 yearly from normal shopping. TopCashback offers similar returns with a £10 sign-up bonus. The trick? Install the browser extension, check before every online purchase. Premium memberships (£1 monthly) add 10% extra cashback.

Banking apps revolutionized saving without trying. Monzo’s 12.1 million UK users love the round-up feature – every card payment rounds up to the nearest pound, spare change earning 3.25% interest. Heavy users accumulate £300+ yearly just from coffee and lunch purchases.

VoucherCodes research shows households earning over £120,000 save £408 annually through voucher use. It’s not about being cheap – it’s leaving money on the table if you don’t. HotUKDeals crowdsources the best offers. Compare the Market gives insurance customers 2-for-1 cinema tickets and meals all year.

Brexit’s Permanent Price Shock Demands New Strategies

Food inflation hit 5.1% in August 2025, highest since January 2024. The LSE calculated Brexit caused one-third of food price rises since 2019, adding £7 billion to national grocery bills. That’s £250 per household that’s never coming back (Bloomberg/LSE study, 2023).

Current inflation sits at 3.8% (ONS Consumer Price Inflation, August 2025). Housing costs for owner-occupiers rose 8% annually. Despite wages growing 5.9%, real growth after inflation is just 1.2-2.1%. The Office for Budget Responsibility projects income growth of only 1% through 2030. The poorest households will be 8% worse off by 2029-30 than in 2019-20.

Healthy food costs more than twice as much per calorie – £8.80 versus £4.30 per 1,000 kcal (Food Foundation, February 2025). These prices rose 21% between 2022-2024, while less healthy options increased just 11%. A family prioritizing nutrition faces an extra £2,000 yearly food bill.

The Joseph Rowntree Foundation reports 66% of families with children are behind on bills, averaging £1,380 in arrears. Their tracker shows 5.3 million households cutting meals, 7 million going without essentials. Resolution Foundation analysis confirms the 2020s will see zero improvement in disposable incomes – a lost decade for living standards.

Making Your Savings Work Instead of Rotting

Easy-access savings hit 4.75% with several providers. Trading 212 offers 4.38%, Santander Edge Saver 5% for existing customers. Fixed rates reach 4.53% for one year. Yet the average UK savings account pays just 1.5% – millions haven’t switched since opening their account.

ISAs remain the no-brainer for tax-free saving. The £20,000 annual allowance per person means couples can shelter £40,000. Cash ISAs pay up to 4.38%. New rules let you open multiple ISAs of the same type annually – spread your risk across providers.

Junior ISAs accept £9,000 yearly per child, earning around 4% tax-free. By 18, maximum contributions plus growth could hit £200,000+. Children can earn £18,570 annually tax-free by combining allowances, though parental gifts over £100 interest get taxed at parent’s rate.

Premium Bonds dropped to 3.6% prize rate but remain popular. Two monthly millionaires, complete capital protection, instant access. Not optimal returns but beats most high-street savings accounts. Maximum holding is £50,000 per person.

Help to Save deserves its own mention again. The 50% bonus is unbeatable – save £50 monthly, get £600 bonus after two years, another £600 after four. Combined with optimal ISA use, a family could generate £2,000+ yearly from savings alone.

The Reality Check

Spending £663 a week for a family of four doesn’t leave much room for changes. Unclaimed benefits, loyalty tweaking, food waste applications, and even good savings accounts can yield massive savings, £3000 to be exact, for a family in the UK while unchanged lifestyle savings are in the thousands.

To begin, the biggest wins. If you haven’t checked the Tax-Free Childcare eligibility, do so. That’s £2000 for each child. If you qualify, Apply for Council Tax Reduction. Switch to the social broadband. Make sure you sorted your Warm Home Discount. That right there are four things that can save you £1500+.

Let the shopping revolution begin. Aldi for the bulk of your shopping, and for add-ons use loyalty cards. If you want variety you can use Too Good To Go. For other items, consider yellow stickered things. Realistic saving from shopping revolution should be about £1000 a year.

Lastly, do the right things to save. For your savings, switch to accounts that offer 4.75% interest, use ISAs in the right way, and if eligible claim Help to Save. Even with £3000 in savings you should be earning £140+ a year at a proper interest rate.

Finding the best savings rates becomes crucial when every pound counts. A family stashing away £200 monthly at 4.75% versus 1.5% gains an extra £780 over three years – enough for a decent holiday or emergency fund boost.

The cost of living crisis is going to stick around for a while. Brexit’s impact is here to stay. Inflation is still high. However, UK families have access to tools and support that they can actively use to shield themselves from the worst problems. They can also establish a support system for anything that comes next.

More References

- Coram Family and Childcare Trust (2025). Childcare Survey 2025 (https://www.coram.org.uk/news/childcare-survey-2025/)

- GOV.UK (2025). Benefit and Pension Rates 2025 to 2026 (https://www.gov.uk/government/publications/benefit-and-pension-rates-2025-to-2026/)

- Which? (2025). Supermarket Price Comparison (https://www.which.co.uk/reviews/supermarkets/article/supermarket-price-comparison-aPpYp9j1MFin)

- Joseph Rowntree Foundation (2025). Cost of Living Tracker Summer 2025 (https://www.jrf.org.uk/cost-of-living/jrfs-cost-of-living-tracker-summer-2025)

- ONS (2025). Consumer Price Inflation UK: August 2025 (https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/august2025)

- Food Foundation (2025). Food Prices Tracker: February 2025 (https://foodfoundation.org.uk/news/food-prices-tracker-february-2025)

- Resolution Foundation (2025). The Living Standards Outlook 2025 (https://www.resolutionfoundation.org/publications/the-living-standards-outlook-2025/)

- Bloomberg/LSE (2023). Brexit Caused a Third of UK Food Price Inflation (https://www.bloomberg.com/news/articles/2023-05-24/brexit-caused-a-third-of-uk-food-price-inflation-lse-paper-says)

{kind=link}