Insurance costs are a major headache for UK drivers and the Association of British Insurers reckons the average motor premium was £551 in Q3 2025 – £56 less than the same quarter in 2014, but still a big chunk of change in most households’ budget. The right comparison site really can save you hundreds of pounds each year – thouehc the key to doing so is knowing which platforms actually produce results, and not just recycle the same quotes over and over.

Comparison sites allow you to check several insurers at once or scour the market, rather than calling around like it is 1995. You could pull dozens of quotes in a matter of minutes, which sounds patently obvious but way too many people continue to renew by default and pay what’s effectively a loyalty penalty. The catch is that not all the comparison sites work with the same insurers, so if you use several you are best positioned to find the lowest price.

Worth knowing:

- Not every insurer appears on every comparison site because some have exclusive deals with specific platforms, which is why checking multiple sites matters

- Comparing doesn’t touch your credit score since sites use soft searches that leave no footprint on your file

- You can compare as often as you like without any negative consequences, so there’s no reason not to check a few weeks before renewal and then again closer to the date

Car Insurance Comparison Sites Worth Using

| Comparison Site | Key Features | Best For |

|---|---|---|

| Clean Green Cars | 110+ providers, specialist EV cover | All drivers, especially electric vehicle owners |

| Compare the Market | Meerkat rewards programme | Quick comparisons with lifestyle perks |

| Confused.com | Price index tracking, Rewards+ scheme | Understanding market trends |

| MoneySuperMarket | Advanced filtering, customer reviews | Detail-focused shoppers |

| GoCompare | Detailed policy charts | Side-by-side comparisons |

Clean Green Cars

Clean Green Cars runs comparisons across 110+ insurance providers, which puts it among the broader panels available to UK drivers. They’ve carved out a niche in specialist cover — standard car insurance sits alongside electric vehicle policies, temporary cover, and business insurance options. The platform grew from a greener motoring resource back in 2016 into a full comparison service, and they operate through Quotezone’s backend which handles the actual quote aggregation.

What works:

- Broad specialist coverage spanning business, temporary, and personal needs

- You can get quotes without a registration number if you’re still deciding on a vehicle

- Potential savings up to £518 based on their June 2025 data, though individual results vary wildly depending on your profile

Worth noting: They’re not a household name like Compare the Market or Confused.com, which means less brand recognition but the underlying comparison mechanics work the same way. The savings claims use averages, so your mileage will differ — sometimes literally.

Compare the Market

Compare the Market delivers results quickly and throws in Meerkat Rewards when you purchase through their platform, which adds genuine value beyond just the insurance quote itself.

The rewards breakdown (12 months after purchase):

- 25% off dine-out bills at participating restaurants

- 50% off pizza delivery from Domino’s (£30 minimum), Papa Johns and Pizza Hut Delivery (£25 minimum)

- 2-for-1 cinema tickets every Tuesday and Wednesday

- 25% off drinks and pastries at Caffè Nero

What works:

- App-based rewards that multiple household members can use

- Extends beyond dining into cinema and coffee perks

- Qualifying products include car, home, pet, travel insurance plus broadband, energy switches, and mobile contracts

Worth noting: Rewards expire after 12 months unless you purchase another qualifying product to top them up. Restrictions apply on bank holidays, Valentine’s Day, and certain promotional periods — the app shows exclusions before you book. Scotland excludes alcohol from dine-out discounts, and you’ll need to mention Meerkat Meals when booking restaurants.

Confused.com

Confused.com holds the distinction of being the UK’s first insurance comparison platform, launching back in 2001 when comparing prices still meant phoning around or trudging between high street brokers. They’ve built out a price index that tracks premium movements across the market, which proves useful for understanding whether you’re getting a fair deal relative to current trends.

Rewards+ programme details:

- £20 eGift voucher redeemable with 100+ brands including Tesco, Sainsbury’s, and Amazon

- Free Greggs hot drink every month for 12 months (regular size, claimed via app)

- Must claim within 60 days of purchase through the Confused.com app

- Maximum £200 in rewards within any 6-month period

What works:

- Transparent premium tracking helps with timing your purchase and renewal

- Regular research updates on cost trends across demographics and regions

- The Rewards+ scheme adds tangible value without complicated redemption hoops

Worth noting: Their strength lies more in data and market intelligence than policy customisation. If you want granular filtering options, MoneySuperMarket might suit better. The Greggs drinks only work through the app — no in-store redemption without it.

MoneySuperMarket

MoneySuperMarket founded by Simon Nixon built their platform around filtering tools that let you sort by price, cover level, and customer ratings simultaneously. If you’re the type who reads reviews before committing to anything, this platform caters to that approach.

What works:

- Comprehensive customer review integration so you can see how insurers perform on claims handling

- Granular filters speed up finding policies that match specific requirements

- Their Electric Car Insurance Index tracks EV-specific pricing trends

Worth noting: The interface can feel cluttered if you’re after a quick comparison without the deep-dive options. Some niche providers get excluded by certain filter combinations, so broadening your search occasionally surfaces options you’d otherwise miss.

GoCompare

GoCompare leans into policy transparency with comparison charts showing exactly what each quote includes and what optional extras cost on top. This helps when you’re trying to compare apples with apples rather than being surprised by excess levels or missing cover after purchase.

What works:

- Strong emphasis on highlighting policy exclusions before you buy

- Straightforward comparison without reward schemes complicating the decision

Worth noting: They don’t offer loyalty incentives or rewards programmes, so the value proposition is purely about finding the right policy rather than earning perks. The quote process sometimes asks for more details upfront than other platforms.

Factors That Influence Your Premium

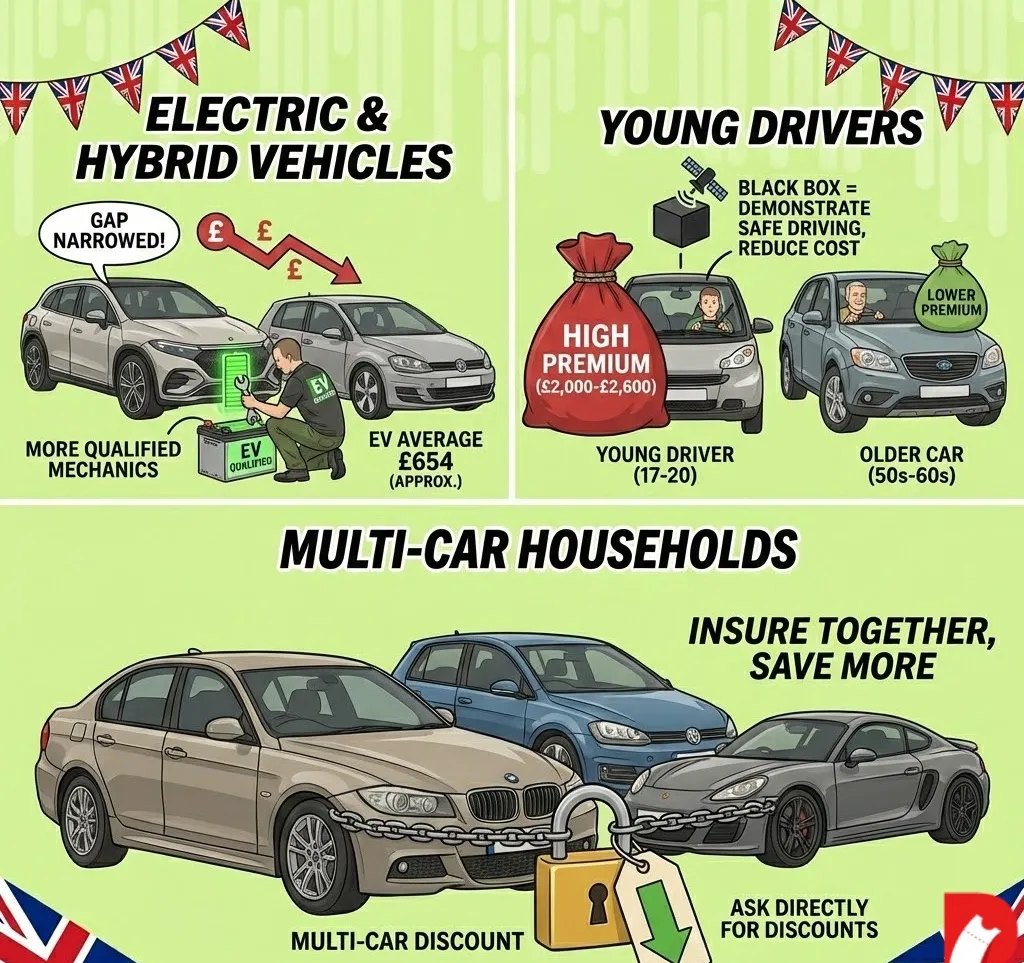

Electric and Hybrid Vehicles

EV insurance costs an average of £654 for popular models in 2025 based on NimbleFins analysis although the cost spans between around £400 and over £1000 depending on the specific motor and your profile. Insurance for an EV versus a petrol car is becoming much closer than it used to as more and more mechanics have completed training on electric vehicles and insurers have seen better claims data.

Repair and battery technology costs still mean EV premiums nudge ahead for now over their petrol equivalent, but the gap is no longer chasm-like as it was a few years ago. For specialist advice on electric vehicle cover, Clean Green Cars optionally offers its own EV comparison tool and LV= and Saga each provide the option of dedicated EV policy features such as chargepoint recovery and cable cover.

Young Drivers

Premiums for new drivers remain at a premium compared to the market, yet 2025 has seen some form of respite with prices falling up to 23% year-on-year for younger age groups. According to the latest stats, drivers who are aged 17-20 now pay an average of between £2,000 and £2,600 a year depending on whose figures you’re looking at — Confused. com puts the figure at roughly £2,031 for that bracket while Uswitch quote data exceeds it by a few hundred pounds at £2,376 for 16-20 year olds.

It comes down to methodology. Confused.com tracks policies actually bought, while Uswitch analyses the quotes being requested and people can generally buy for less because they shop around and take discounts. Either way, young motorists pay several times what someone in their 50s or 60s would for the same cover.

Black box policies (telematics insurance) are still the best way to cut these costs, as they allow you to prove you drive well, rather than simply pricing on age-based risk. The trade-off there is being tracked while driving, but for drivers confident in their abilities it can shave large chunks off the premium.

Multi-Car Households

That number can be as much as 24 percent if you have more than one car to insure, though there is upsell built into this and not all comparison sites will always offer these options up front in a transparent way on the page. Worth asking directly if you’re comparing for multiple cars — the discount is there but you sometimes have to push for it.

Tips to Trim Your Insurance Costs

- Compare 3-4 weeks before renewal: Premiums tend to be lower when you’re shopping with time to spare rather than scrambling at the last minute. Insurers know desperation when they see it.

- Pay annually if you can swing it: Monthly payments include interest charges that add 15-25% to your total cost over the year. If cashflow allows, the annual lump sum works out cheaper despite the initial sting.

- Adjust voluntary excess carefully: Raising your excess lowers premiums, but make sure you can actually afford to pay it if you need to claim. A £500 excess saving you £80 annually looks less clever when you’re scraping together the payment after an accident.

- Add named drivers strategically: Experienced drivers with clean records can bring your premium down, but the main driver must genuinely be whoever uses the car most. Fronting — listing a parent as main driver when it’s actually their child’s car — is fraud and insurers actively look for it.

- Never auto-renew without checking: Insurers routinely charge existing customers more than new ones, banking on inertia. The ten minutes spent comparing before renewal pays for itself repeatedly.

Beyond Price: What Else Matters

The cheapest policy isn’t automatically the best choice, and a penny wise approach here can prove pound foolish when you actually need to claim. Excess amounts deserve particular scrutiny — a policy might look attractively priced but carry a £1,000 excess that makes smaller claims pointless.

Check before buying:

- Policy coverage details — Basic policies sometimes exclude windscreen damage, courtesy cars, or breakdown cover that you might assume comes standard

- Customer service ratings — How an insurer handles claims matters enormously when you’re dealing with the stress of an accident. Reviews from actual claimants tell you more than marketing copy

- The full policy document — Summary pages highlight selling points but the actual terms contain exclusions and conditions worth understanding before you’re locked in

- Total excess — Compulsory plus voluntary combined gives you the real figure you’d pay towards any claim

An insurer that’s difficult to deal with during a claim adds stress to an already rubbish situation. Sometimes paying slightly more for a provider with better claims handling saves you hassle that’s worth more than the premium difference.

The Bottom Line

Car insurance prices have dropped from their 2023/24 peaks but remain elevated compared to pre-pandemic levels. Using multiple comparison sites gives you the broadest view of what’s available, and the differences between platforms mean checking two or three genuinely surfaces different options rather than wasting time.

Start comparing 2-3 weeks before your renewal date with your current policy details to hand so you can match cover levels accurately. Even a brief comparison session often saves hundreds annually — the ABI’s £551 average means plenty of drivers pay more, and those overpaying tend to be the ones who don’t shop around.

Your circumstances shift and so do insurance prices. What was competitive last year might not be this year, and the insurer who gave you a decent deal previously has no obligation to do so again. Treat comparison as an annual habit rather than a one-off task and you’ll consistently pay closer to market rate rather than whatever your current provider fancies charging.

Sources:

- Association of British Insurers Motor Insurance Premium Tracker, Q3 2025

- NimbleFins Electric Car Insurance Analysis, 2025

- Confused.com Car Insurance Price Index, Q3 2025

- Uswitch UK Car Insurance Statistics, 2025

{kind=link}